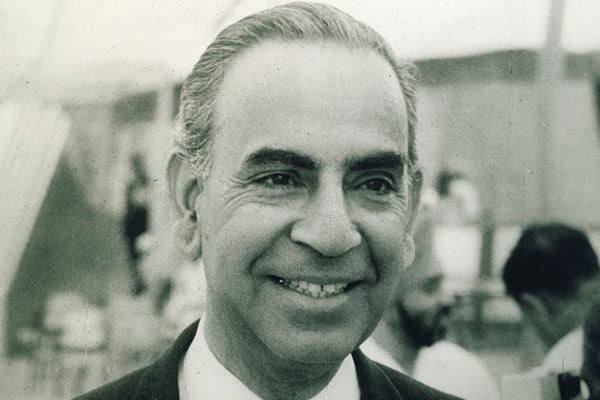

Report of the Study Group to Frame Guidelines for Follow-up of Bank Credit (1975), chaired by Prakash Tandon

Download as PDF

In the early 1970s, India faced significant economic challenges, including rising inflation, stagnant industrial production, and mounting pressures on bank resources. The nationalization of major commercial banks in 1969 had aimed to democratize credit distribution, but the cash credit system at the time continued to prioritize large industries over small-scale enterprises, agriculture, and newer sectors. Amidst these inefficiencies, the Reserve Bank of India established a Study Group in July 1974 under the chairmanship of Prakash Tandon, Chairman, Punjab National Bank, to propose reforms and frame guidelines for more effective supervision and utilization of bank credit. Members included S. K. Bhattacharyya (Indian Institute of Management); P. P. Dhir (Director (Finance), Minerals and Metals Trading Corporation of India Ltd.); A. Ghosh (General Manager, Allahabad Bank); T. S. Kannan (Managing Director, Richardson & Cruddas (1972) Ltd.); R. C. Maheshwari (General Manager, Texmaco Ltd.); P. B. Medhora (Joint Managing Director, Industrial Credit and Investment Corporation of India Ltd.); P. K. Nanda (Managing Director, Metal Box Company of India Ltd.); S. Padmanabhan (Chief Officer, Commercial and Institutional Banking, State Bank of India); Sampat P. Singh (Faculty Member, National Institute of Bank Management); Y. V. Sivaramakrishnayya (Assistant General Manager, Bank of Baroda); A. K. Bhuchar (Joint Chief Officer, Department of Banking Operations and Development, Reserve Bank of India); P. J. Fernandes (Additional Secretary and Director General, Bureau of Public Enterprises, Ministry of Finance); N. Rajan (Adviser (Finance), Bureau of Public Enterprises, Ministry of Finance); and N. C. B. Nath (Director (Commercial), Steel Authority of India Ltd.).

The study group identified several flaws in the prevailing banking system. The cash credit system allowed borrowers to draw funds unpredictably, leading to resource mismanagement and speculative hoarding. By mid-1974, sanctioned credit limits exceeded deposits (INR 12,880 crores against INR 10,706 crores), straining the banking sector. Furthermore, the absence of standardized norms for inventory and receivables encouraged overfinancing in some industries while others were underserved.

To address these issues, the group recommended replacing the cash credit system with a structured model, comprising term loans and demand cash credit, supported by quarterly budgeting and monitoring. Industry-specific norms for inventory and receivables were proposed, covering sectors such as textiles, fertilizers, and pharmaceuticals, to ensure efficient use of working capital. Banks were advised to finance no more than 75% of the working capital gap, requiring borrowers to contribute long-term funds to encourage financial discipline. Flexibility in norms was permitted under exceptional circumstances, such as supply chain disruptions or delayed government payments, but banks were urged to adopt a robust credit monitoring system to prevent misuse.

The report also emphasized reducing speculative activities and aligning credit allocation with developmental goals. It encouraged banks to prioritize productive sectors, improve supervision, and enhance transparency through a streamlined information system. At the central level, the Reserve Bank of India adopted key recommendations, including the suggested methods for assessing Maximum Permissible Bank Finance (the amount of working capital requirement a bank could finance), industry-specific inventory norms, bifurcated cash credit limits, and improved reporting systems.

By phasing in these reforms, the study group envisioned a banking system that would promote equitable growth, optimize resource utilization, and meet the evolving needs of a dynamic economy.